Theory vs. Practice

Monday, January 13, 2020

Written by Nathan Polackwich, CFA

Categories: PASI Stocks General Markets and Economy

A client recently asked about the relatively focused nature of our portfolio, curious as to why we hold fewer stock positions than many other investment managers. Currently, the PASI portfolio owns 32 stocks (diversified by industry) and one Exchange Traded Fund (ETF) tracking the Oil and Gas sector of the S&P 500. Each of these 33 positions comprises somewhere between 2% and 4% of the overall portfolio. How did we arrive at this portfolio structure?

There are two ways to approach an infinitely complex problem like the stock market.

- Start with a theory of how the system works and apply the processes you believe will perform best.

- Learn, through practice/experience, what works (and what doesn’t) and refine your processes over time.

Method 1 is only useful for closed and simple systems. For instance, you can fix a washing machine just by studying how it works and then using what you’ve learned without experience. But in far more complex domains with infinite variables – like the economy, financial markets, politics, health, etc. – naïvely applying theories is almost always a recipe for disaster. In that case, Method 2 – refinement through practice/experience – is the wiser path.

The distinction between these two approaches – theory vs. practice – has long been recognized. In his Histories, the ancient historian, Polybius, when comparing the Spartan legislator Lycurgus to Rome observed that Lycurgus, “by a process of reasoning, whence and how events naturally happen, constructed his constitution untaught by adversity.” Conversely, the Romans didn’t develop their government “by any process of reasoning, but by the discipline of many struggles and troubles, and always choosing the best by the light of the experience gained.” While Sparta was a regional power in Greece for a few hundred years, Rome endured for a millennium, exercising hegemony over the entire Mediterranean (and beyond) for much of that time.

Roman practicality and the Greek affinity for theory are even apparent in their philosophers. The trader and author Nassim Taleb notes in Antifragile how the great Roman thinker, Seneca, “focused on the practical aspect of Stoicism,…mostly, how to handle adversity and poverty and, even more critically, wealth…Other philosophers, when they did things, came to the practice from theory. Aristotle, when he attempted to provide practical advice, and a few decades earlier Plato, with his ideas of the state and advice to rulers, particularly the ruler of Syracuse, were either ineffectual or caused debacles. To become a successful philosopher king, it is much better to start as a king than as a philosopher.”

The development of the PASI stock portfolio has been far more “Roman” than “Greek” in orientation since the firm’s founding in 1977. Our investment process has evolved as lessons have been learned and markets have changed. Earlier in our history we owned both fewer and more positions in the stock portfolio than the current 33. But we ultimately arrived at this number because it provided the optimal blend of diversification, positive impact from good ideas, and limited downside from bets that didn’t pan out as hoped.

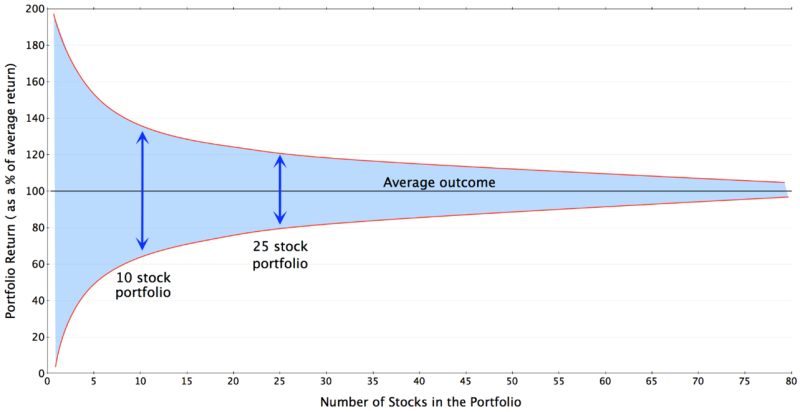

Interestingly, the economic literature (theory!) now supports our portfolio structure. The following chart shows the probability of matching the stock market averages as you add stocks to a portfolio. Note that at 25 positions, a stock portfolio captures the vast majority – about 80% – of the benefits of diversification.(1)

Why not try to be 100% rather than 80% diversified? One issue is that the more stocks you include, the lower your odds of achieving above-average results. As an extreme example, it would be impossible for us to outperform if we bought all 500 stocks in the S&P 500 index.

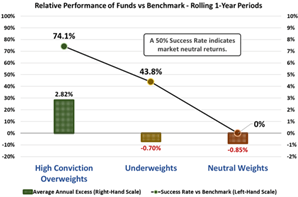

Holding just 33 positions also allows us to concentrate on our best ideas. This focus matters because studies show that active investment managers’ high conviction stocks – those they overweight in their portfolios – strongly outperform the stock market averages.(2)

Most active investment managers have stock-picking skill. But they dilute the benefit of their high conviction ideas by allocating money to less attractive stocks in the name of increased diversification. At PASI we’ve found that owning about 33 stocks helps us avoid this drag while simultaneously obtaining most of the risk-reducing benefits of diversification.

In addition to a more focused portfolio, we’ve refined our investment process in numerous other ways. For instance, many years ago we noticed that poorly performing stocks often take much longer to recover – if they ever do – than investors anticipate. Accordingly, we put strict limits on the money we’ll add to an underperforming stock. (In investment parlance adding more and more money to a declining stock has been dubbed “catching a falling knife.”)

The converse to the falling knife is a stock advancing much farther and faster than you ever imagined. This is a good problem to have! But it presents a challenge for disciplined investors because overvaluation dampens a stock’s long-term return. Even a great company will be a lousy investment if you pay too high a price.

How do we handle such a scenario? We’ve learned it’s usually a good idea to hang in there when a stock’s performance exceeds our expectations (within reason). Often, it turns out the Company is growing faster – and therefore worth more – than we originally thought. Moreover, while troubled companies usually take a long time to turn their businesses around, successful companies with strong competitive advantages can thrive indefinitely. And PASI determined early on that it’s precisely these kinds of companies that make the best long-term investments.

A stock may appear inexpensive relative to its earnings or book value, but that doesn’t necessarily mean it’s a good opportunity. Auto maker Ford illustrates this phenomenon well.

Ford’s stock almost always appears “cheap” relative to its earnings. But those earnings – and therefore its stock – never achieve lasting gains because Ford operates in a slow-growing, extremely competitive industry. The result is a stock that’s been highly volatile but ultimately has been dead money for the past three decades.

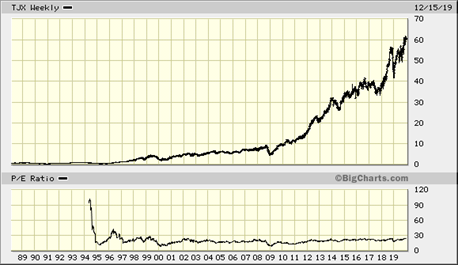

In contrast to companies like Ford, at PASI we look for “compounders” or durable businesses that operate in expanding markets and can grow their earnings year after year. A great example is PASI holding TJ Maxx (TJX), a terrific business that’s proven to be a compounding machine.

This is the kind of performance a growing business with sustainable competitive advantages can achieve. Notice how TJX’s Price/Earnings ratio (bottom chart) remained steady throughout most of the stock’s meteoric rise – Earnings have risen right in line with the share price! While not every PASI stock will perform this well, TJX is a prime example of the kind of high-quality company we’ve come to prefer. And this policy – like all our investment decision-making processes – is the product of more than four decades of constant refinement and adaption.

Sources:

1) Newbould, Gerald & Poon, Percy. (1996). Portfolio Risk, Portfolio Performance, and the Indvidual Investor. The Journal of Investing. 5. 72-78. 10.3905/joi.5.2.72.

2) Panchekha, Alexy, CFA (2019). The Active Manager Paradox: High-Conviction Overweight Positions. https://blogs.cfainstitute.org/investor/2019/10/03/the-active-manager-paradox-high-conviction-overweight-positions/.